News

Blockchain technology meets munis in Quincy, Massachusetts

Enjoy complimentary access to top ideas and insights — selected by our editors.

Transcription:

Transcripts are generated using a combination of speech recognition software and human transcribers, and may contain errors. Please check the corresponding audio for the authoritative record.

Michael Scarchilli (00:05):

Hi everyone, and welcome to the Bond Buyer podcast, your go-to source for all things municipal finance. I’m Michael Scarchilli, editor-in-chief of the Bond Buyer. And this week we are taking a hard look into how issuers are tapping technology to both transact in the market and think about how to use tech tools to more effectively and efficiently run the business of the government. In a first of its kind transaction, in April, the city of Quincy, Massachusetts issued $10 million of tax exempt bonds using blockchain technology. Taking the first step in what those involved in the transactions say could be a game changer for the muni bond market. Quincy Mayor Tom Koch, CFO, Eric Mason and strategic asset manager Rick Coscia, talked to Bond Buyer, executive editor Lynne Funk about why Quincy decided to test the waters with the transaction, how they think it will provide cost savings, liquidity, and more access for retail investors. They also discuss how Quincy is finding ways to lure in a younger generation of public finance government employees in a time when state and local governments are finding the effort challenging. And with that, let’s get started and dive into this week’s conversation.

Lynne Funk (01:22):

So I would love to kick this off. You had a really interesting transaction back in April. It was $10 million of debt issued using the blockchain technology distributed ledger technology, which is a collection of digital systems that record transactions in multiple locations almost simultaneously. Mayor Koch, I would love you to kick us off here. Can you just tell our listeners about how you came to decide to price this first of its kind deal? Why did you do it? How did you do it?

Thomas Koch (01:53):

Well, first of all, we do a lot of bonding in the city. We get a healthy budget. We’re an old city, so we’re been updating our infrastructure, whether it’s buildings or pipes or roads, a lot of great projects, a lot of public infrastructure updates that had been long overdue. So we were in the market frequently on a number of projects, including new schools. We get reimbursements from the state. I depend heavily on Eric Mason and Rick Coscia who advise me on timing of these things. The way to go about it, what are the options are for the city, what makes sense and the newer world that we’re moving into, this seemed to make sense to give it a shot. So $10 million is a low number for us actually, but we thought it was a good number to try this out.

Lynne Funk (02:40):

Great. Eric, would you want to kind of talk a little bit about how you structured this? How did this deal get done? Who was involved? Yeah,

Eric Mason (02:47):

Yeah, absolutely. Obviously it comes from top-down approach. So yeah, it’s a conversation. I mean, all bonding is, well, bonding is certainly financial, but certainly policy setting too. Additionally, city council president Ann Kain was a big advocate of this, but in terms of structuring an individual deal, it was kind of unique. We have a really, really good team involved in this both internally and externally. So Rick Coscia obviously leading up the bond efforts in addition to even Mike Roland too as a financial operations manager, because think of it this way, everything we bond has to be deployed. So that’s always be concert between the barring action and the implementation action. But externally, Hilltop Securities is their financial advisor. We have Locke Lord, who was invaluable bond counsel. Then also working with JPM, I mean it’s their product and their platform. Additionally, we had Blockwise come on as advisors for this is the first time we’re doing a blockchain bond in the United States.

(03:49):

It’s good to have experts who understand the underlying technology, but overall, I mean it’s a team effort inside and out in terms of structuring the actual deal to market. Rick can get a little more into that, but it was really about matching the maturity to where the demand of the market is. But as an economist, it’s always hard when you have a new market to figure out where demand is. So it was very interesting. It was a very interesting conversation. We really put the negotiated into negotiated debt when it came to this. But Rick, do you want to jump into a little bit of the structure itself, sir?

Rick Coscia (04:17):

Yeah, absolutely. So I think the mayor kind of made the most salient point on this in that it made a lot of sense for Quincy to do this because we have such frequent issuers. So if you are a small community and you don’t go to market a lot, you’re probably not going to be that interested in it because you don’t go to market as much. You’re not going to see, ultimately what we’re hope to see is lower transaction costs and enhanced liquidity and just more efficient transaction in the equity market’s a little bit easier. If you want to buy a stock or you want to invest, there are plenty of platforms, there’s plenty of buyers and sell. The municipal market’s a little bit different. The secondary market is really important, so it’s a lot less efficient, meaning to buy and sell, you have to, it’s more of a niche market.

(05:08):

So being a frequent issuer that we go to the market so frequently we knew this is something we wanted to look at because when you issue a bond, you’re incurring issuance costs, you’re incurring transaction costs, you’re paying third party intermediaries like your underwriters and your financial advisors and your bond counsel and any other consultants. So ultimately I think the reason we did this was because we see this as the future. There’s no arguing that this is going to be the way transactions are done, maybe not next year, maybe not in two years, but ultimately that’s the way that this is going to go, just like any other investment transaction. So we want to be part of it. The mayor is always tasking us to say, ‘look, can we do things more efficiently? Can we do things better? Can we save money? Is there ways of doing this in a better way?’

(05:54):

So we went forward with it. In terms of how we structured it, again, we wanted to dip our toe in the market a little bit. It was a $10 million deal. As Mayor Koch said, it’s a lot of money, but in the big scheme of things, in the big picture, it’s not. But for the city, we just recently we’re going got authorization for $157 million to do a couple of new parking garages for a development in our downtown, and we wanted to do it in a way that wouldn’t have a negative impact to our budget. So we structured it in a way that’s a seven year maturity. So we looked at the numbers and we made sure the principal and interest wouldn’t have, like I said, a deleterious effect on our budget. And listen, we got a lot of guides, Eric and I would like to think we’re the smartest guys in the room and we’re not.

(06:42):

But we got a lot of guidance from our financial advisors, from JP Morgan. It was their platform. So they took the entire deal down themselves. They took the $10 million down them themselves. While they’re doing that though, they were also building out the secondary market, their platform. So to buy these bonds, you had to be on JP Morgan’s Onyx platform and they have several large investment managers that are in the process of doing that. But we wanted to be first, we’re in a better situation, a better situation than a lot of other communities and a lot of other deals that are in play now. And I think one of the questions you’ll probably ask is we were the first, are there any other deals going on? And there are, but we wanted to be first and we were able to do that, like I said, with our consultants help as well as JP Morgan’s help. So hopefully that answered your question.

Lynne Funk (07:29):

It does. I think, can you go a little more granular here though? I’m just curious in terms of how does this type, how does blockchain transaction provide cost savings for issuers like yourself?

Eric Mason (07:42):

It’s two part. So the first one is whenever you break down barriers, you have the effect of barriers are expensive, it’s inherent nature of financial barriers. So by breaking out barriers and democratizing the process, even as something as, it’s funny, I was on Bloomberg, I refer to municipal bonds as boring, and one of the hosts of the close is like, oh, they’re great, they’re tax free income, all this stuff. But sometimes it’s hard to find efficiency in the boring because it’s been so optimized. I mean, find something more regulated than municipal borrowing. So that’s why great advance. When you have something that’s as structured as municipal debt, it takes great advancements to create return. So by breaking down these barriers, we make it a lot less expensive to enter the market. And having the reporting mechanism tied to the financial vehicle the entire time means RERE reporting, which is a very expensive process, is optimized to a point where it’s not like every time you sell this bond, it has to be rerecorded, it has to follow the same paper trail.

(08:44):

The paper is always attached to, which is also much safer. But the second portion is, and certainly the economic side of it, is that when you open up the market, you have more demand. And when you have more demand and you have fixed supply, people are willing to incur a higher price to buy the bond and a higher price to the buyer is a lower price to us, the seller. So there’s the economics of it, which is fascinating. And the finance side of it, it’s just a better product. It’s the same reason why we don’t sell physical savings bonds anymore. But yeah, it’s

Rick Coscia (09:20):

The only thing I would add, Lynne, is as you know, we do a bond deal, we’ll sell a hundred million dollars worth of bonds and it’s always the usual suspects that buy our bonds. I mean, it’s going to be institutional investors, it’s going to be a mutual fund companies, it’s going to be insurance companies and investment managers. And a small portion of that will also be separately managed accounts. SMAs and in those SMA are high, high net worth clients. So those are the ones that typically buy our bonds. And one of the things I think the may probably talk about this is that one of the things we wanted to do, or the tasks that he asked us to look into is the democratization of this, right? So if you are a constituent in Quincy and you see a new public safety building going up, but we’re selling bonds for that.

(10:06):

We’ve had conversations with people like, gee, I would’ve liked to have, I live in Quincy. I’m going to live my whole life in Quincy. I see the development going on in the city. I’d like to have kind of invested in some of the infrastructure that you’re doing here. This overtime is going to allow that. Where again, when we do a hundred million dollars, that deal is usually over subscribed for six, eight times within the first couple hours. So a lot of those, I guess the retail investors, the retail bond buyers, they kind of shut out of this. This ultimately will open that up. So

Lynne Funk (10:36):

We’re talking right now, I’m an investor. I live in Quincy. I don’t have $5,000 for a bond. Maybe I have a thousand, maybe I have 500. Is that why the goal is with this type of transaction where you open up the universe to the retail investor who maybe doesn’t have the $50,000, democratizing the amount of bonds that they can purchase?

Eric Mason (10:59):

Yeah, yeah, absolutely. That’s the long-term goal is this technology works on the penny par and it works on 5,000 par, the 50,000 par we want. See, one of the things the blockchain is that because of its association with crypto, its association with technology, a lot of traditional investors are turned off to it because the complexity to learn it can sometimes be daunting. But what’s funny is that there’s no new, I always said there’s no new economics. Economics is nothing new under the sun. What we see now as we reduce that par, say we reduce it down to the penny, that’s no different than what happened between exporting countries and importing countries exporting nations want really, really low value of currency because it creates an advantage and import export. Same thing here. The city who is exporting this debt wants the lowest units possible because that makes it easier to sell than the open market.

(11:53):

There’s no loss of value. We’re just changing the unit. And to have that ability to change the unit, and the only thing stopping that unit change for the last a hundred, 200 years was that the reporting requirement to be able to actually generate the note and secure and do all that was quite costly. It required a lot of expertise where now we can digitize that. So similar like sending an email, you get the same information in an email as you do in mailing a letter, but you do it for free. That’s really that democratization side of it that we’re looking to engage with

Thomas Koch (12:27):

I, which is pretty cool. I mean, we do financial literacy programs in the high schools and we’d like to do more of it, but at some point we’ll have these discussions in there and I think that will help young people understand the whole idea of what the market is all about when it comes to the bonding. I know Rick used the reference of the public safety headquarters run our fifth new school. I think the Squam Elementary School will be one that I think some people would love to be part of, whether it’s a 500 bucks or a grand or 10 grand to be in it because they either attended it, their kids are going there, it’s just there’s this connection they would have to their own commute. I think it’s pretty exciting. So we’re looking forward to that next step. Excellent.

Rick Coscia (13:10):

Just one thing real quick. You talked about where the cost savings act, one of the aspects is really, it’s really blunt. It’s you’re going to have less parties involved. So when we get to that point where you want to be an investor you want to invest in or purchase bonds that are going to fund the new Squam Elementary School right now, you have to either go through the underwriters, you have to go through who that underwriter is to sell you those bonds going forward. Once you’re on that platform, once, if you were on the JP Morgan platform, you would’ve been able to buy those bonds directly. You wouldn’t have to have gone, and the issuer doesn’t have to go sell those bonds through the underwriter. They can sell ’em directly from that platform. So it just ultimately over time, we’ll cut out that middleman. And if you’re cutting out middleman, then you’re ultimately cutting out costs too and you’re seeing savings, and that’s a long game on it.

Lynne Funk (14:04):

Excellent. So I have to ask you, mayor Koch, did this somewhat stem from, you host Quincy, Massachusetts host a blockchain event? Can you talk about that? It’s broader, it’s outside of Munis. Is that kind of where this all came from or is it come together at the same time?

Thomas Koch (14:21):

Probably in part, I mean our council president, Ian Kain is heavily involved in that world and advocates that all the time. I’ve got the best municipal finance department around. These guys are on top of everything, new technology. That’s not my world. I hire the best and listen. So yeah, so I get a lot to learn in that whole world. But Eric and my team, I mean Rick and the whole team, they dive into these things. They become expert on it. They get the outside help and we need the help on these things. But yeah, I mean that whole blockchain, the president of the council invited me down to do some opening remarks and first time they had it, and I think I said something along the lines is, I don’t know what you do. I know why I am here, but I know really what the hell you guys do, but I hope you have a great week. Welcome to Quincy. So I’ve learned a little bit more since then, but I’m at that age where some of the stuff is a little intimidating, but there’s hope for even me, but the world is changing and we’ve got to be part of that.

Lynne Funk (15:28):

Right. So you’re saying mayor, that perhaps Eric and Rick are being humble and they are the smartest guys in the room

Eric Mason (15:34):

In your group? Absolutely know I’m not. No, just ask my wife

Thomas Koch (15:39):

Not on every issue, but certainly they serve me well serve the city well.

Lynne Funk (15:47):

Excellent. So can you talk about perhaps, and I’ll open this up to you all, how does FinTech figure into, factor into city planning? How technology, how FinTech, what are you all focused on right now in terms of that?

Eric Mason (16:06):

Yeah, so the word FinTech has just evolved so much over the last 10, 15 years. I remember when I first started in college, the idea of FinTech was this marriage between your financial operations and your IT department, but now it’s turned into everything from smart streets. I very much appreciate the mayor’s compliments on municipal finance, but always trying to learn and grow. But I’ll tell you, some of the departments, especially like T pal, just traffic parking alarm and lighting, the team over there, I mean they really thought of that integration into bringing technology onto everything. We see it in our fire department with bringing on software that firefighters are going to fight fires, they’re pulling out iPads that are tied into the permitting software so they know what the buildings look like. And this just goes on and on and on in terms of this detail.

(16:55):

But when we talk about FinTech integration in the larger form, if we just talk about traditional definition within finance and technology, the IT director for the city, Ryan is really somebody that I’ve come to love working with and we’ve always had a string of good IT directors, but it’s that marriage where you understand that there is no such thing as a separate finance software and a separate technology stack, that your tech stack is your financial operations now. And there’s something called a toll bear model in government. Basically government’s always 20 years behind in technology. It’s like an old economic model that people used to reference and yeah, it’s true government’s behind and that’s why it’s strange that especially from a policy standpoint through the mayor, that government was the first to do a blockchain deal in the United States, especially outside of the 5 0 3 and 5 0 6 processes.

(17:45):

So what FinTech looks like to us is I would describe it as ubiquitous and invasive. It’s always trying to be stacked together to get the greatest force multiplier. When we first brought in our ERP, it was underutilized and it made it very painful to use. But one of the things the mayor has done over time is not just engage in that ERP or bring on experts using that ERP to integrate through it. And there’s also a little time factor. I mean, having younger people coming into the workforce who are used to ERPs means major FinTech. Your FinTech approach can be much more aggressive because people are more used to using the software. But having that nice marriage of institutional knowledge flowing through the application into the FinTech, into the overall accounting structure you can create with a well and matured industry and workforce, really effective usage. It’s not just a software to me, it’s not just software. It’s software and people. You combine those two together, it’s really impressive what can be generated.

Rick Coscia (18:48):

Yeah, one byproduct, I would say through the whole adoption of FinTech and blockchain technology is something that weaves its way into every transaction. It’s the security element of it right now. It’s a very manual, believe it or not, it’s not sure working for bond buyer, I’m sure this, it’s a very manual archaic way of selling securities, which when is very manual and archaic, it can lend itself to mistakes, it can lend itself to potential fraud, and blockchain is kind of tightens up that transaction chain. So the only people that can take part in that transaction are those who have been approved and any change has to be approved by everyone on that blockchain. So that I think was a really a big important part of it as well. I mean municipalities is seeing it if companies are seeing the fraud and there being cyber acts and things like that. And this again is just one more step in terms of just making sure the city is secure and how we do business and how we transact bond sales is much more secure.

Lynne Funk (19:59):

That’s an interesting point you bring up, Rick, because when you say cyber, how does blockchain, how does it deter cyber or how does it protect cybersecurity for transactions?

Eric Mason (20:13):

Yeah, I mean it’s a scale game. The ability to break a blockchain, I mean there are probably countries that don’t have that level of computing power. Realistically, everything gets overtaken by everything, right? There’s always going to be a new technology. There’s always going to be a faster car, faster rocket, but there are just upper limits and it’s a resource game. If you look at cybersecurity like a war, the wars are won through resources. Even with some of the modern cubic level quantum computers, even at 50 qubits, you’re really becoming towards the upper limit of being able to break and sustain a break of a blockchain. That’s the key here. When our treasurer Molly Smith, who’s also absolutely valuable in this process, we’re very lucky to have very, she comes from a private sector background. Again, Quincy Paris lives in the city, but she handles, she’s the one who sends out the millions of dollars of debt payment every year, and she was vital in this process.

(21:15):

And when we first were on the Onyx platform and she was going through it, every time she moved the cursor, clicked on a new thing to look at the bond, it was re-engaging that it’s one thing to hack into a system. It’s one thing to break a vault, nothing to hold a vault open. And seeing that in there and realizing just the monumental power it would take to create fraud in this system, to get inside of it and manipulate it, that’s reassuring. It’s like sitting inside of a tank. It’s not just safer drivers, it’s a safer product. So I think that’s a big one. In the second one, I’m going to give kind of a boring answer. When we pay bonds, we bring out the wires. They have to be up by 10:00 AM They have to be US bank for distribution after that by 2:00 PM or you get a paper default with blockchain technology because the ledger is decentralized, everybody knows who is owed everything. It just comes, it’s like a direct deposit I should say.

Thomas Koch (22:10):

Is that a Sherman tank or an Abrams tank?

Eric Mason (22:12):

I prefer the Abram. I think there’s more reactive armor on it, but yeah, it comes right out the account, you’re paying your water bill. There’s no risk of a paper default, which I know is a little different from the cybersecurity, but it’s still a concern.

Rick Coscia (22:29):

No, that was another element, the enhanced liquidity. We get those funds in because those funds are used a lot of times, whether it’s DPW or some of these other departments, they’re depending on those funds to pay their contracts for the work that’s being done. That is going to be done, and the turnaround time is much more efficient. We’re going to see those funds in a lot, I think it was several days as opposed to usually it takes us over, can take us seven to 10 days for those funds to come in. That was definitely shrunk down. And I’ll just say, I’m kind of repeating myself, but something the may have said earlier is that we’re in the market a lot. I can’t stress it enough that Eric and I are in the market so often because we have such an aggressive agenda, and that’s because of the guy in the corner, right hand, right hand corner that we have such an aggressive agenda and really the city has gone through a renaissance over the last 15, 17 years that it makes sense we’re a perfect candidate for this type of transaction because we’ll see this savings over time.

(23:27):

If you’re just issuing once or twice a year, yeah, maybe it’s like, look, we’ll, we’ll just do it the old way. We don’t care. We don’t go to the market that often, but it’s the law of returns the more often you’re in the market. It makes sense for you to look for ways to kind of do those transactions and be more efficient in that work.

Lynne Funk (23:46):

So how far away are you all from doing a hundred million? From doing 200 million? How far away are other issuers from replicating this? I guess I’m just curious. Is it a matter of just people dipping their toes and doing it or,

Eric Mason (24:01):

Yep. We’re already seeing the trend Europe, we’re already seeing these larger issuances going through. It’s about everybody getting comfortable with it. I was at a conference shortly after, actually the day we got the funding for this, I was at a conference in New York talking about this, and Lynne, you hit the question on the head. That’s exactly what was asked me because I’m sitting front, it’s a conference. I was pretty much all CFOs and so they’re all like, I’m kind of interested in this. And it felt very bizarre because CFOs, we tend to be the most financially conservative people, an organization as a public sector, CFO. I should have been the most conservative person in a room full of conservative financial individuals. So talking about blockchain was actually kind of funny, but no, I mean the skill works, it goes up. Siemens did a massive one.

(24:44):

I mean Switzerland, who we worked closely with their CFO, it’s scalable. The thing is about getting comfortable, and here’s why I think government hit it first. It’s what the mayor said. We have different incentives. We’re trying to bring the lowest cost and democratize the debt. So the Squam schools got a hundred million dollar note. If the mayor wants to aim it for that a hundred million and let’s democratize this, we can start setting up a strategy for that. I don’t think there’s an upper limit to the scale on here. I think it works on the 10 million. I think it’ll work on the a hundred million.

Rick Coscia (25:16):

I think you’ll look, you’ll see some when we were going through our process and we had to go through a pretty lengthy process to get all the regulatory hurdles overcome. But on the corporate side, I know we’re on the municipal side, but you’ll see corporate deals over a billion dollars. Eric mentioned the one in Switzerland, but you’re going to see, yeah, I mean you’ll easily see billion dollar deal.

Lynne Funk (25:39):

Europeans definitely are typically ahead of the US in these types of things.

Rick Coscia (25:44):

Well, their regulatory requirements, let’s just say little more. Let’s use the word flexible than the us. I like the spa, but you won’t see a billion dollars in cleansing. We sure about that. No.

Lynne Funk (26:02):

Well, this is a good little segue for a second to kind of talk about Quincy itself. The city itself. You are what, 11 miles south southeast of Boston? Boston has center.

Thomas Koch (26:14):

Yeah, center. The center. I mean we border Neponset River together.

Lynne Funk (26:18):

Got it. Boston has had its fair share of challenges from commercial real estate vacancies, transit ridership, drops, but far as I can tell, it looks like Quincy’s economy has bearing been faring quite well. Do you want to get into why that is? I would love to hear it.

Thomas Koch (26:35):

Okay. A couple of things. One is I think Quincy was one of the best kept secrets for a long, long time. I mean location, proximity to Boston, four stops on the red line commuter rail ferry, 27 miles a coastline. We are about the seven or 8,000 acres of blue hills, all kinds of opportunities. Safe city, great school system. I could go on and on. The school is, schools are thriving, the city’s thriving in so many ways, but at the end of the day, in my early years when things were a little bumpy financially, it took office, the financial meltdown began and we had to get a fiscal house in order. If you don’t have your fiscal house in order, then the schools aren’t going to be what they can be. We can’t maintain a infrastructure like we should. So getting that the financial household rental was huge, and this team has been tremendous in doing that.

(27:28):

So we’ve got a good reputation in the marketplace. People like to buy our debt. There’s a reason for that and we are thriving. We didn’t get caught up in commercial. We’ve been doing a lot of residential, which is, as you know, there’s a great shortage for housing stocks for people in the greater Boston area, and we’ve been embracing that. We’re between six and 7,000 units since I’ve been there, which has pretty hefty, but it’s been awesome and it’s provided additional tax revenue. It provides jobs for the construction portion of it. I mean, it could go on and on. We have a great city with the seventh largest city of Massachusetts, and I would argue since we’ve reorganized our government, created new departments, we are acting like a city our size now, and that includes the municipal finance department at all. They’re doing

Lynne Funk (28:16):

How large is the city? I actually, I’m sorry, I forget.

Thomas Koch (28:20):

Well, we’re 17 square miles, but the population by federal counts about a hundred thousand, 2000. I would argue we’re probably closer to 110, 112 maybe we truly can count it, but the attics and boiler rooms and things, but we will leave that alone. But again, we’re seventh largest. I think we’re 14th largest in New England, but as an urban area, we get the lowest crime rate. One of the same for an urban school district. We are very successful. Kids do very well in this district. We spend a lot of effort and time in making sure those kids have that opportunity to succeed. So I’m very proud to serve as mayor. The city is really grown. We’ve reclaimed our history. Next couple of years we’re going to go on the ground for a new Adams presidential center to really speak to the history of this country, and it all started right here in many cases by the hand and pen of John Adams. So we’ve got a remarkable road and we’re just getting going.

Lynne Funk (29:19):

So you’re telling me with all this housing stock, you’ve got some retail investors out there.

Thomas Koch (29:25):

Oh, absolutely. When you have the housing stock, it leads to a lot more retail.

Lynne Funk (29:34):

So actually just as another quick aside here, I did want to pivot over to a topic that is I think I’m hearing so much about, and that is that state and local governments are having challenges with hiring for people such as Eric and Rick in terms of the government getting finance folks in. There’s a shortage of accountants, there’s a shortage of just people interested, young people, particularly in getting into public finance, getting into government,

Thomas Koch (30:00):

I guess. Yeah, that’s one of the areas and we’re really focused on, we’re building a great farm system here. I’ve got a lot of young people, Eric … Rick’s not so young, but Eric falls in that category of the young guys. Colleen Haley who I brought on, she was the youngest chair of the assessors in the history of the city. She did a remarkable job turning things around, and many of our departments are now infiltrated with a lot of young people. A lot of young people don’t think about government, they really don’t coming out of school. But when it’s exposed to them and they’re part of something because it’s not just going to work nine to five and going, well, no, you see what you’re involved in day-to-day in the life of a city. When you’re part of the government here, you’re part of the case of talk a lot about bonding.

(30:51):

So Rick and Eric, they drive by that school. Hey, they were part of a financing of that building. I mean, it really gives greater buy-in, especially if you come from the community and you love the community, you feel like you’re contributing, you feel like you’re being part of something that’s much greater than yourself. And I think as we’ve exposed a lot of young people to this, they’ve bought in and one of the challenges with some communities is paying the help they need to pay as well. And we have upgraded our department managers department heads to a level that’s far more competitive. That’s another aspect of it, but we’re getting a lot of work done and we’re having a lot of fun

Eric Mason (31:27):

As a product of that farm system daily. I’ve always joke about two jobs in my life, both on Hancock Street. I pumped gas at my family’s gas station and then I’ve worked for city hall. So I worked at 819 Hancock and I worked at 1305 Hancock Street. Yeah, I was brought on at 21. I don’t know if you thought this is how this is going to turn out, but plus

Thomas Koch (31:49):

I did.

Lynne Funk (31:52):

Eric, may I ask, can you tell our audience how old you were when you were tapped? A CFO?

Eric Mason (31:58):

Yes. I was 26. I

Lynne Funk (31:59):

Thought so, yeah,

Eric Mason (32:01):

About a year before I came on, I wasn’t allowed to rent a car and that was fun. Best thing about being as young as I was, I could ask so many stupid questions. It was awesome. One of the things that the mayor did when he came on is that he rebuilt a lot of our relationships, like our independent auditors, our independent financial arms. So Jim Powers, who is the city’s auditor, independent auditor, one of the most well-respected minds and the entire, definitely in the state, but probably in the country because I’ve been in conferences with him for us CPA stuff, not just Mass CPA. He and I got along great. He actually grew up pumping gas, also comes from a blue collar of family like me and May would just send me down to his office and be like, alright, go talk to Jim and Wakefield, figure out how, learn the tax rate, learn auditing and all that stuff.

(32:53):

And I was like, I’m a little brother. I know I missed the forest through the trees a lot. But having the opportunity when you’re young to basically sit there and be like, I’m going to ask you a lot of dumb questions, a lot of dumb questions. We do a lot of smart answers. That’s definitely one thing I learned in this job, but being part of that farm system because it’s a supportive environment and I don’t think you get that a lot in government. I don’t think you get that a lot in the private sector either where you have the CEO of the city of the mayor taking time to work with the farm system to work with the young kids, encourage the mistakes being made. I always tell that to my interns. I’m like, make mistakes. You’re not need to cure cancer, make mistakes. You’re going to fall down.

(33:29):

We’re going to pick you right back up because that’s what the mayor did for me. So who am I to do something different than that? And you end up building this really robust system. Mike Roland, who’s our financial operation manager’s office, is just on the other side of that wall. Same thing. He was an intern when he was 18, 19 years old, and now he builds the budget for the city and they become committed to it. If you could see that little cardboard box, I know we’re on a podcast, so let’s do, but there’s a little card poster board the mayor to run the head. It’s different than this. We’re $500 million a year budget. We have 1.3 billion in current assets. It doesn’t even include our ability to tax is 290 million a year. I don’t even if you propagate that further down the road, that’s a huge operation.

(34:12):

I always say this, if you have a company doing 41 million a year on revenue in your city, your expenditures, that’s a big company. That’s just our police department, just our police department. We are spending half a billion dollars out on the streets and it’s mostly local. We employ over 4,000 people. This is the conglomerate, but do what I enjoy. My favorite project I’ve ever done, we’ve done the pension obligation bond. That was amazing. The blockchain bond, that was amazing. There’s all these great projects. We’ve done the learning Center, which is a special needs school. I know the mayor can dive into a lot more in detail than me. That’s what that poster board is. That’s what I keep in my office. I keep those poster boards. That was my favorite project we’ve ever done because at the end of the day, this type of financial knowledge, I went to a big state school.

(34:54):

I have friends all over doing crazy stuff with finance that is interesting to me. But what I think it’s cool is that we could take these towns and I took it to city. I grew up in my family. I grew up on Ry. I grew up five and a half miles from where the gas station I worked at and I sit there. I went to Quincy Public Schools and now knowing that there’s a building and the mayor saw an old former candy factory, I think it was Johnson’s Candy Factory a little bit before my time boss, and it got turned into a place that can house educate 300 kids with autism spectrum disorder. But I think of that the next step. I mean they’re going to do speech therapy there. I was in speech therapy for seven years of my life. I had a law of promise with speech, still have a law of promise with speech, but they’re going to do physical therapy, occupational therapy, and I think do what I think of these kids get on this bus.

(35:47):

They have to go an hour out to some school an hour back. One of the things the mayor has kept here is we have neighborhood schools. So now those kids can go to school in the morning, get their PT and OT they need and their speech therapy and their specialized care in district then go back to their schools. Those kids are forming friendships that when they move to high school are statistically shown to not just increase their rate of their rate of graduation, but their education, their mental health, little stuff like that. I’m sorry, you’re not getting on the private sector. They could pay you more. They could do all that stuff. And as Mary said, we went through more than a couple of compensation analysis in the last couple of years. It’s competitive, but that is a lot of happiness and utility to be able to use the stuff you studied in school and the stuff you wanted to specialize in and what do you get to use it for? Making sure special needs kids have a better life. Come on. That’s not something you’re getting in the private sector. And I saw a broke record, I said that to anybody who’s looking in the local side. I’m like, can’t beat that.

Rick Coscia (36:43):

Well, I had a little bit of a not different perspective, but yeah, in terms of my perspective, I came from the private sector. I was in the private sector 25 years on investment management. And coming in I thought, well, to be honest with you, I was like, I’m going from private sector to government. Am I going to be bored? And so I worked with the mayor and I met a bunch of times and it has been, I’ve been pleasantly surprised how ambitious and this city is run like a large corporation in a good way. I mean, we have ambitious goals. Those goals are kind of communicated and we’re given the tools to carry out those goals and to execute them. And so again, you talked about young people coming into government that’s attractive and I know I’m going to pay the mayor a compliment even though he called me old. But I think that all comes from the vision of the CEO.

(37:44):

I’ve lived in Quincy my entire life, born and bred here. I’ll probably die here. And I have over the last 15 to 17 years, the city has just gone through this. I keep using the word, the Renaissance, this revitalization. There’s so much pride going on and he’s right. I’ll go out driving with my wife and we actually drove by the Chris building last night on the way back from the in of Bay Point. And yeah, it’s kind of cool saying, I grew up here, I was born here and I worked here, and we helped in a little way of carrying out the vision of building five new schools, of seeing the total redevelopment of the downtown, of new public safety buildings, new roads and sidewalks. It’s a really cool place to live. It may me using this analogy, but it’s the same thing that’s happened to a lot of these other communities like the Somerville and the Cambridges, and these were not cool places to live 20 years ago.

(38:41):

They were punchline. Like I said, now they have some of the most popular places to live. The market values reflect that, and that’s what’s really, there’s just this pride of of home that you’ve seen in the city that it’s just tangible. And I think that’ll be attractive to young people. Believe me, I get a lot of calls from friends who are like, listen, I’m ready to make that jump. Is there anything happening in the city? And I don’t think that was the case 10, 15 years ago. You’re right. I think it was like, well, I don’t work the city. This debate will be different. I won’t be doing as many cutting edge things. At least that’s not the case in Quincy. I mean, I’m fairly new to the municipal side, but I’ve been pleasantly surprised. It’s been great.

Lynne Funk (39:26):

It’s definitely, that’s good to hear. I think sometimes we see a lot of negative headlines and I think these are sort of positive ones to share and share with the industry itself. And so many times some people say, I’m stealing this from someone. I can’t remember who. But that you don’t find munis, they find you.

Thomas Koch (39:45):

No, that’s true.

Lynne Funk (39:47):

But that we want to maybe change that and really get, I think a story. Your stories are a good way to tell the story of public finance and why it matters and how it can be. You can be part of your life. Very quick though. I got to tell you said this. It’s really funny. And then we are going along here, but Eric, you and I have something very much in common, and that is my first job was at a gas station.

Lynne Funk (40:12):

Job. I did not pump gas. I was a sandwich shop gal at 15 or 16, at a family of friend’s, locally owned gas station in Pittsburgh, Pennsylvania. Then I went to college and then I moved to New York and I got into munis somehow. So they found me. But mayor, all three of you, but Mayor Koch, is there anything that we didn’t ask you, I didn’t ask you that you wanted to leave the listeners with?

Thomas Koch (40:40):

I think we get it covered. Actually. I’m heading down running a little late. I’m heading down the cut the ribbon for the farmer’s market opens up today for the summer, so I got to head down there and say hello to that team. But no, I appreciate you having us on and Quincy’s open for the business for those people out there listening and we’ll, we’re going to continue to be trailblazers when it comes to all the tools out there, the municipal finance side of things, and I get the best in these guys. So thanks for having us.

Lynne Funk (41:10):

Thank you so much for being here on all of you.

Thomas Koch (41:13):

Thank you.

Michael Scarchilli (41:15):

We hope you enjoyed this episode. A big thank you to Mayor Koch, Eric Mason and Rick Coscia for joining us and to our own Lin Funk for conducting the interview.

Let’s review some key takeaways from this conversation.

One, while they do not think it will happen overnight, Quincy officials believe their $10 million blockchain deal could be the start of a trend in the muni market. Once more issuers realize how it can save them money and give more investors access to their deals.

Two, the officials believe that technology will also allow more local retail investors the opportunity to access their deals at denominations smaller than the current norm of $5,000 and three, Quincy has focused on engaging a younger generation of talent, particularly those in the city itself, to show them why working in government is not only a noble profession, but a fun, engaging, and lucrative one too. Quincy’s own CFO, Eric Mason started working for the city at 21 and was promoted to CFO at 26.

Thanks again for listening to this Bond Buyer podcast. This episode was produced by the Bomb Buyer. If you enjoyed this episode, please hit like and subscribe on your favorite podcast player and please rate us, review us and subscribe to our content at www.bombbuyer.com/subscribe. Until next time, I’m Mike Scarchilli signing off.

The attack, which exploited a vulnerability disclosed in April, drained around 60 million ASTRO tokens, sending the price plummeting.

The Terra blockchain has been exploited for over $6 million, forcing developers to take a momentary break the chain.

Beosin Cyber Security Company reported that the protocol lost 60 million ASTRO tokens, 3.5 million USDC, 500,000 USDT, and 2.7 BTC or $180,000.

Terra developers paused the chain on Wednesday morning to apply an emergency patch that would address the attack. Moments later, a 67% majority of validators upgraded their nodes and resumed block production.

The ASTRO token has plunged as much as 75%. It is now trading at $0.03, a 25% decline on the day. Traders who took advantage of the drop are now on 195%.

ASTRO Price

ASTRO PriceThe vulnerability that took down the Cosmos-based blockchain was disclosed in April and involved the deployment of a malicious CosmWasm contract. It opened the door to attacks via what is called an “ibc-hooks callback timeout reentrancy vulnerability,” which is used to invoke contracts and enable cross-chain swaps.

Terra 2.0 also suffered a massive drop in total value locked (TVL) in April, shortly after the vulnerability was discovered. It plunged 80% to $6 million from $30 million in TVL and has since lost nearly half of that value, currently sitting at $3.9 million.

The current Earth chain emerged from the rubble as a hard fork after the original blockchain, now called Terra Classic, collapsed in 2022. Terra collapsed after its algorithmic stablecoin (UST) lost its peg, causing a run on deposits. More than $50 billion of UST’s market cap was wiped out in a matter of days.

Terraform Labs, the company behind the blockchain, has been slowly unravelling its legal woes since its mid-2022 crash. Founder Do Kwon awaits sentencing in Montenegro after he and his company were found liable for $40 billion in customer funds in early April.

On June 12, Terraform Labs settled with the SEC for $4.4 billion, for which the company will pay about $3.59 billion plus interest and a $420 million penalty. Meanwhile, Kwon will pay $204.3 million, including $110 million in restitution, interest and an $80 million penalty, a court filing showed.

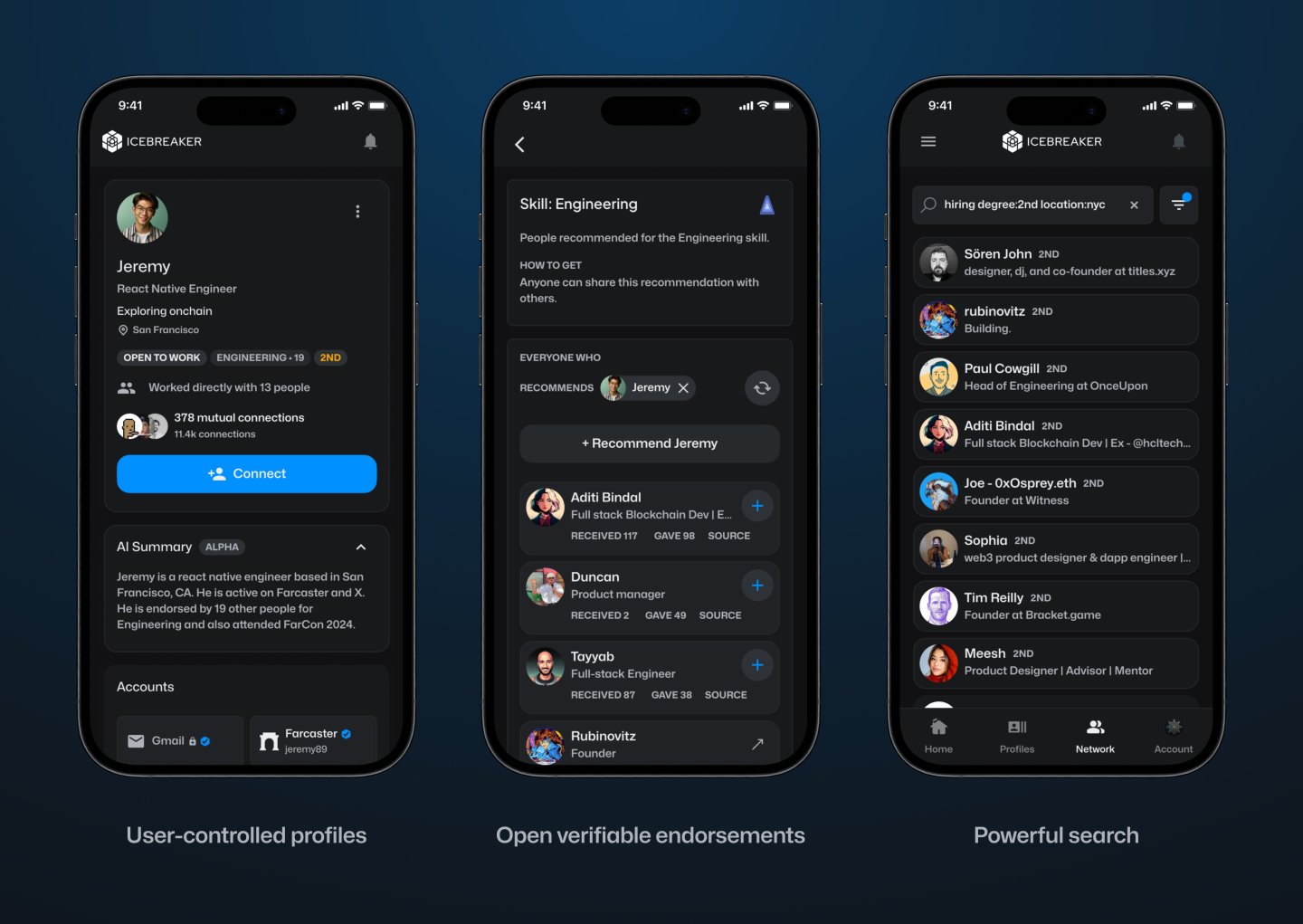

Icebreaker: Think LinkedIn but on a Blockchain—announced Wednesday that it has secured $5 million in seed funding. CoinFund led the round, with participation from Accomplice, Anagram, and Legion Capital, among others.

The company, which is valued at $21 million, aims to become the world’s first open-source network for professional connections. Its co-founders, Dan Stone and Jack Dillé, come from Google AND Monetary base; Stone was a product manager at the cryptocurrency giant and also the co-creator of Google’s largest multi-identity measurement and marketing platform, while Dillé was a design manager for Google Working area.

The pair founded Icebreaker on the shared belief that the imprint of one’s digital identity (and reputation) should not be owned by a single entity, but rather publicly owned and accessible to all. Frustrated that platforms like LinkedIn To limit how we leverage our connections, Dillé told Fortune he hopes to remove paywalls and credits, which “force us to pay just to browse our network.” Using blockchain technology, Icebreaker lets users transfer their existing professional profile and network into a single, verified channel.

“Imagine clicking the login button and then seeing your entire network on LinkedIn, ChirpingFarcaster and email? Imagine how many introductions could be routed more effectively if you could see the full picture of how you’re connected to someone,” Stone told Fortune.

Users can instantly prove their credentials and provide verifiable endorsements for people in their network. The idea is to create an “open graph of reputation and identity,” according to the founders. They hope to challenge LinkedIn’s closed network that “secures data,” freeing users to search for candidates and opportunities wherever they are online. By building on-chain, the founders note, they will create a public ledger of shared context and trust.

Verified channels are now launched for

Chirping

Online Guide

Wallet

Discord

Telephone

TeleporterYou can find them in Account -> Linked Accounts Italian: https://t.co/mRDyuWW8O2

— Icebreaker (@icebreaker_xyz) April 3, 2024

“Digital networking is increasingly saturated with noise and AI-driven fake personas,” the founders said in a statement. For example: Dillé’s LinkedIn headline reads “CEO of Google,” a small piece of digital performance art to draw attention to unverifiable information on Web2 social networks that can leave both candidates and recruiters vulnerable to false claims.

“Icebreaker was created to enable professionals to seamlessly tap into their existing profiles and networks to surface exceptional people and opportunities, using recent advances in cryptographically verifiable identity,” the company said, adding that the new funding will go towards expanding its team and developing products.

“One of the next significant use cases for cryptocurrency is the development of fundamental social graphs for applications to leverage… We are proud to support Dan, Jack and their team in their mission to bring true professional identity ownership to everyone online,” said CoinFund CIO Alex Felix in a statement.

Learn more about all things cryptocurrency with short, easy-to-read flashcards. Click here to Fortune’s Crash Course in Cryptocurrency.

Fuente

On July 24, 2024, the Ministry of Finance proposed Blockchain Bill IVwhich will provide greater flexibility and legal certainty for issuers using Distributed Ledger Technology (DLT). The bill will update three of Luxembourg’s financial laws, the Law of 6 April 2013 on dematerialised securitiesTHE Law of 5 April 1993 on the financial sector and the Law of 23 December 1998 establishing a financial sector supervisory commissionThis bill includes the additional option of a supervisory agent role and the inclusion of equity securities in dematerialized form.

DLT and Luxembourg

DLT is increasingly used in the financial and fund management sector in Luxembourg, offering numerous benefits and transforming various aspects of the industry.

Here are some examples:

- Digital Bonds: Luxembourg has seen multiple digital bond issuances via DLT. For example, the European Investment Bank has issued bonds that are registered, transferred and stored via DLT processes. These bonds are governed by Luxembourg law and registered on proprietary DLT platforms.

- Fund Administration: DLT can streamline fund administration processes, offering new opportunities and efficiencies for intermediaries, and can do the following:

- Automate capital calls and distributions using smart contracts,

- Simplify audits and ensure reporting accuracy through transparent and immutable transaction records.

- Warranty Management: Luxembourg-based DLT platforms allow clients to swap ownership of baskets of securities between different collateral pools at precise times.

- Tokenization: DLT is used to tokenize various assets, including real estate and luxury goods, by representing them in a tokenized and fractionalized format on the blockchain. This process can improve the liquidity and accessibility of traditionally illiquid assets.

- Tokenization of investment funds: DLT is being explored for the tokenization of investment funds, which can streamline the supply chain, reduce costs, and enable faster transactions. DLT can automate various elements of the supply chain, reducing the need for reconciliations between entities such as custodians, administrators, and investment managers.

- Issuance, settlement and payment platforms:Market participants are developing trusted networks using DLT technology to serve as a single source of shared truth among participants in financial instrument investment ecosystems.

- Legal framework: Luxembourg has adapted its legal framework to accommodate DLT, recognising the validity and enforceability of DLT-based financial instruments. This includes the following:

- Allow the use of DLT for the issuance of dematerialized securities,

- Recognize DLT for the circulation of securities,

- Enabling financial collateral arrangements on DLT financial instruments.

- Regulatory compliance: DLT can improve transparency in fund share ownership and regulatory compliance, providing fund managers with new opportunities for liquidity management and operational efficiency.

- Financial inclusion: By leveraging DLT, Luxembourg aims to promote greater financial inclusion and participation, potentially creating a more diverse and resilient financial system.

- Governance and ethics:The implementation of DLT can promote higher standards of governance and ethics, contributing to a more sustainable and responsible financial sector.

Luxembourg’s approach to DLT in finance and fund management is characterised by a principle of technology neutrality, recognising that innovative processes and technologies can contribute to improving financial services. This is exemplified by its commitment to creating a compatible legal and regulatory framework.

Short story

Luxembourg has already enacted three major blockchain-related laws, often referred to as Blockchain I, II and III.

Blockchain Law I (2019): This law, passed on March 1, 2019, was one of the first in the EU to recognize blockchain as equivalent to traditional transactions. It allowed the use of DLT for account registration, transfer, and materialization of securities.

Blockchain Law II (2021): Enacted on 22 January 2021, this law strengthened the Luxembourg legal framework on dematerialised securities. It recognised the possibility of using secure electronic registration mechanisms to issue such securities and expanded access for all credit institutions and investment firms.

Blockchain Act III (2023): Also known as Bill 8055, this is the most recent law in the blockchain field and was passed on March 14, 2023. This law has integrated the Luxembourg DLT framework in the following way:

- Update of the Act of 5 August 2005 on provisions relating to financial collateral to enable the use of electronic DLT as collateral on financial instruments registered in securities accounts,

- Implementation of EU Regulation 2022/858 on a pilot scheme for DLT-based market infrastructures (DLT Pilot Regulation),

- Redefining the notion of financial instruments in Law of 5 April 1993 on the financial sector and the Law of 30 May 2018 on financial instruments markets to align with the corresponding European regulations, including MiFID.

The Blockchain III Act strengthened the collateral rules for digital assets and aimed to increase legal certainty by allowing securities accounts on DLT to be pledged, while maintaining the efficient system of the 2005 Act on Financial Collateral Arrangements.

With the Blockchain IV bill, Luxembourg will build on the foundations laid by previous Blockchain laws and aims to consolidate Luxembourg’s position as a leading hub for financial innovation in Europe.

Blockchain Bill IV

The key provisions of the Blockchain IV bill include the following:

- Expanded scope: The bill expands the Luxembourg DLT legal framework to include equity securities in addition to debt securities. This expansion will allow the fund industry and transfer agents to use DLT to manage registers of shares and units, as well as to process fund shares.

- New role of the control agent: The bill introduces the role of a control agent as an alternative to the central account custodian for the issuance of dematerialised securities via DLT. This control agent can be an EU investment firm or a credit institution chosen by the issuer. This new role does not replace the current central account custodian, but, like all other roles, it must be notified to the Commission de Surveillance du Secteur Financier (CSSF), which is designated as the competent supervisory authority. The notification must be submitted two months after the control agent starts its activities.

- Responsibilities of the control agent: The control agent will manage the securities issuance account, verify the consistency between the securities issued and those registered on the DLT network, and supervise the chain of custody of the securities at the account holder and investor level.

- Simplified payment processesThe bill allows issuers to meet payment obligations under securities (such as interest, dividends or repayments) as soon as they have paid the relevant amounts to the paying agent, settlement agent or central account custodian.

- Simplified issuance and reconciliationThe bill simplifies the process of issuing, holding and reconciling dematerialized securities through DLT, eliminating the need for a central custodian to have a second level of custody and allowing securities to be credited directly to the accounts of investors or their delegates.

- Smart Contract Integration:The new processes can be executed using smart contracts with the assistance of the control agent, potentially increasing efficiency and reducing intermediation.

These changes are expected to bring several benefits to the Luxembourg financial sector, including:

- Fund Operations: Greater efficiency and reduced costs by leveraging DLT for the issuance and transfer of fund shares.

- Financial transactions: Greater transparency and security.

- Transparency of the regulatory environment: Increased attractiveness and competitiveness of the Luxembourg financial centre through greater legal clarity and flexibility for issuers and investors using DLT.

- Smart Contracts: Potential for automation of contractual terms, reduction of intermediaries and improvement of transaction traceability through smart contracts.

Blockchain Bill IV is part of Luxembourg’s ongoing strategy to develop a strong digital ecosystem as part of its economy and maintain its status as a leading hub for financial innovation. Luxembourg is positioning itself at the forefront of Europe’s growing digital financial landscape by constantly updating its regulatory framework.

Local regulations, such as Luxembourg law, complement European regulations by providing a more specific legal framework, adapted to local specificities. These local laws, together with European initiatives, aim to improve both the use and the security of projects involving new technologies. They help establish clear standards and promote consumer trust, while promoting innovation and ensuring better protection against potential risks associated with these emerging technologies. Check out our latest posts on these topics and, for more information on this law, blockchain technology and the tokenization mechanism, do not hesitate to contact us.

We are available to discuss any project related to digital finance, cryptocurrencies and disruptive technologies.

This informational piece, which may be considered advertising under the ethics rules of some jurisdictions, is provided with the understanding that it does not constitute the rendering of legal or other professional advice by Goodwin or its attorneys. Past results do not guarantee a similar outcome.

The Department of Veterans Affairs would have to evaluate how blockchain technology could be used to improve benefits and services offered to veterans, according to a legislative proposal introduced Tuesday.

The bill, sponsored by Rep. Nancy Mace, R-S.C., would direct the VA to “conduct a comprehensive study of the feasibility, potential benefits, and risks associated with using distributed ledger technology in various programs and services.”

Distributed ledger technology, including blockchain, is used to protect and track information by storing data across multiple computers and keeping a record of its use.

According to the text of the legislation, which Mace’s office shared exclusively with Nextgov/FCW ahead of its publication, blockchain “could significantly improve benefits allocation, insurance program management, and recordkeeping within the Department of Veterans Affairs.”

“We need to bring the federal government into the 21st century,” Mace said in a statement. “This bill will open the door to research on improving outdated systems that fail our veterans because we owe it to them to use every tool at our disposal to improve their lives.”

Within one year of the law taking effect, the Department of Veterans Affairs will be required to submit a report to the House and Senate Veterans Affairs committees detailing its findings, as well as the benefits and risks identified in using the technology.

The mandatory review is expected to include information on how the department’s use of blockchain could improve the way benefits decisions are administered, improve the management and security of veterans’ personal data, streamline the insurance claims process, and “increase transparency and accountability in service delivery.”

The Department of Veterans Affairs has been studying the potential benefits of using distributed ledger technology, with the department emission a request for information in November 2021 seeking input from contractors on how blockchain could be leveraged, in part, to streamline its supply chains and “secure data sharing between institutions.”

The VA’s National Institute of Artificial Intelligence has also valued the use of blockchain, with three of the use cases tested during the 2021 AI tech sprint focused on examining its capabilities.

Mace previously introduced a May bill that would direct Customs and Border Protection to create a public blockchain platform to store and share data collected at U.S. borders.

Lawmakers also proposed additional measures that would push the Department of Veterans Affairs to consider adopting other modernized technologies to improve veteran services.

Rep. David Valadao, R-Calif., introduced legislation in June that would have directed the department to report to lawmakers on how it plans to expand the use of “certain automation tools” to process veterans’ claims. The House of Representatives Subcommittee on Disability Assistance and Memorial Affairs gave a favorable hearing on the congressman’s bill during a Markup of July 23.

Elon Musk’s X Money is about to change cryptocurrencies FOREVER

Solana Update: 2025 Potential and SOL Price Predictions You MUST SEE!!

Crypto News: Bitcoin BREAKING ATHs, Trump Memecoin, XRP & SOL Flying & More!

China’s $75 billion crypto secret discovered: What it means for you

$500 to $500,000: BIG Cryptocurrency Gains with a SMALL Wallet!?

Crypto News: Bitcoin, ETH Price, CPI Print, PYTH, WIF & MORE!!

Crypto News: Bitcoin Price, ETF, ETH, WIF, HNT & MORE!!

Metasphere Labs announces follow-up event regarding

Solana price potential?! Check out THIS update if you own SOL!!

Who Really CONTROLS THE MARKETS!! Her plans REVEALED!!

Elon Musk’s X Money is about to change cryptocurrencies FOREVER

Solana Update: 2025 Potential and SOL Price Predictions You MUST SEE!!

Crypto News: Bitcoin BREAKING ATHs, Trump Memecoin, XRP & SOL Flying & More!

China’s $75 billion crypto secret discovered: What it means for you

$500 to $500,000: BIG Cryptocurrency Gains with a SMALL Wallet!?

-

Videos9 months ago

Videos9 months agoCrypto News: Bitcoin, ETH Price, CPI Print, PYTH, WIF & MORE!!

-

Videos9 months ago

Videos9 months agoCrypto News: Bitcoin Price, ETF, ETH, WIF, HNT & MORE!!

-

DeFi9 months ago

DeFi9 months agoMetasphere Labs announces follow-up event regarding

-

Videos9 months ago

Videos9 months agoSolana price potential?! Check out THIS update if you own SOL!!

-

Videos8 months ago

Videos8 months agoWho Really CONTROLS THE MARKETS!! Her plans REVEALED!!

-

DeFi6 months ago

DeFi6 months agoPump.Fun Overtakes Ethereum in Daily Revenue: A New Leader in DeFi

-

DeFi6 months ago

DeFi6 months agoDegens Can Now Create Memecoins From Tweets

-

News6 months ago

News6 months agoNew bill pushes Department of Veterans Affairs to examine how blockchain can improve its work

-

News6 months ago

News6 months agoLawmakers, regulators to study impact of blockchain and cryptocurrency in Alabama • Alabama Reflector

-

Bitcoin6 months ago

Bitcoin6 months ago1 Top Cryptocurrency That Could Surge Over 4,300%, According to This Wall Street Firm

-

Ethereum8 months ago

Ethereum8 months agoComment deux frères auraient dérobé 25 millions de dollars lors d’un braquage d’Ethereum de 12 secondes • The Register

-

Videos8 months ago

Videos8 months agoCryptocurrency News: BTC Rally, ETH, SOL, FTM, USDT Recover & MORE!